Substantial Chance Of A Major Financial Collapse Follows The End Of Offshored Industrialization

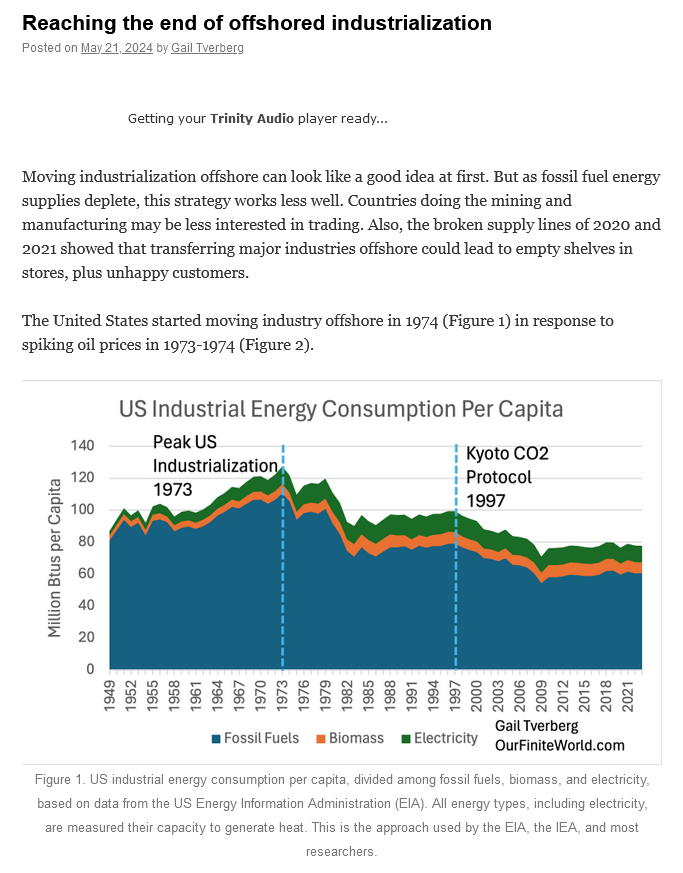

Moving industrialization offshore can look like a good idea at first. But as fossil fuel energy supplies deplete, this strategy works less well. Countries doing the mining and manufacturing may be less interested in trading. Also, the broken supply lines of 2020 and 2021 showed that transferring major industries offshore could lead to empty shelves in stores, plus unhappy customers.

Industry is based on the use of fossil fuels. Electricity also plays a role, but it is more like the icing on the cake than the basis of industrial production. Industry is polluting in many ways, so it was an “easy sell” to move industry offshore. But now the United States is realizing that it needs to re-industrialize. At the same time, we are being told about the need to transition the entire economy to electricity to prevent climate change.

A transition to all electricity is not feasible without fossil fuel ironically. Instead, we seem to be headed for increased geo-political conflict and the possibility of a financial crash seems greater.

Economists and energy analysts have tended to assume that fossil fuel prices would rise to very high levels, allowing extraction of huge amounts of difficult-to-extract fossil fuels. For example, the International Energy Agency (IEA) in the past has shown forecasts of future oil production assuming that inflation-adjusted oil prices will rise to $300 per barrel.

Instead of rising to a very high level, fossil fuel prices tend to spike because there is a two-way contest between the price the consumers can afford and the price the sellers need to keep reinvesting in new fields to keep fossil fuel supplies increasing. Prices oscillate back and forth, with neither buyers nor sellers finding themselves very happy with the situation. The current price of the benchmark, Brent oil, is $81.

When world oil prices started to spike in the 1973-1974 period, the US started to move its industrial production offshore. The very low inflation-adjusted prices that prevailed up until 1972 no longer held. Manufacturing costs climbed higher. Consumers wanted smaller, more fuel-efficient vehicles, and such cars were already being manufactured both in Europe and in Japan. Importing these cars made sense.

More recently, coal prices have begun to spike. Before China joined the World Trade Organization (WTO) in 2001, coal prices tended to be below $50 per ton. At that price, coal was a very inexpensive fuel for making steel and concrete, and for many other industrial uses.

After China joined the WTO, China’s coal consumption soared, allowing it to industrialize. At present, coal prices are part-way back down, perhaps partly because higher interest rates are dampening world demand for coal.